Introduction of Capital Budgeting, PBP and NPV

Capital Budgeting

Initial Investment = $ 30,000

Project - B

Initial Investment = $ 29,000

Calculate PBP.

Solution:

Given that,

Year before full recover = 2

Uncovered Cost =$ 29,000 - $ 21,000

= $ 8,000

Cash flow during the year = $ 9,000

PBP = ?

Hence, the Pay Back Period is 2.89 years.

Capital budgeting is the process that businesses use to determine the merits of investment projects.

Capital Budgeting Techniques

There are two types of techniques in capital budgeting.These are-

1.Traditional Cash Flow Approach

2.Discounted Cash Flow Approach

In Traditional Cash Flow Approach, there have two techniques.These are-

1) PBP (Pay Back Period)

2) ARR (Average Rate of Return)

In Discounted Cash Flow Approach, there have three techniques.These are-

1) NPV (Net Present Value)

2) IRR (Internal Rate of Return)

3) PI (Profitability Index)

PBP ( Pay Back Period )

Pay Back Period (PBP) means how much time need to recover the initial investment.

Decision Criteria

*If PBP < Number of the period, Accept the project.

*If PBP > Number of the period, Reject the project.

Note: Shorter PBP is better.

Advantages

* Easy to calculate and simple to understand.

* Highlights risk.

Disadvantages

* Doesn't consider TVM.

* Doesn't consider Risk.

* Doesn't consider the whole cash flow of the project.

Formula

|

| PBP ( In case of Annuity) |

|

| PBP ( In case of Mixed Cash Inflow) |

Math

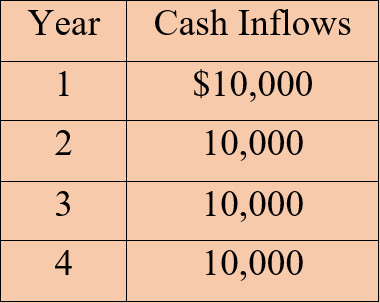

Project - A

Initial Investment = $ 30,000

Calculate Pay Back Period.

Solution:

Given that,

Initial Investment =$ 30,000

Annual Cash Inflow =$ 10,000

Project - B

Initial Investment = $ 29,000

Calculate PBP.

Solution:

Given that,

Year before full recover = 2

Uncovered Cost =$ 29,000 - $ 21,000

= $ 8,000

Cash flow during the year = $ 9,000

PBP = ?

Hence, the Pay Back Period is 2.89 years.

Net Present Value - NPV

Net present value is the difference between the present value of cash inflows and initial investment.

NPV is used in capital budgeting to analyze the profitability of a projected investment of the project.

Decision Criteria

IF,

NPV > 0 , Accept the project.

NPV < 0 , Reject the project.

NPV = 0

Accept the project.Because the value of NPV is positive and have the chance to gain profit in near future.

When there is no scope for investing or there is no profitable project then we can take the project at NPV=0.

Or

We may accept or reject the project.

Merits

* It considers TVM. (Time Value of Money )

* It considers total benefits arising from proposals.

* It helps to achieve the maximization of shareholders wealth.

* It is a direct measure of dollar contribution to stockholders.

*It can handle multiple discount rates without any problem.

Demerits

*The project size is not measured.

*It needs discount factor for calculation.

*It requires some guesswork about the firms' cost of capital.

Comments

Post a Comment